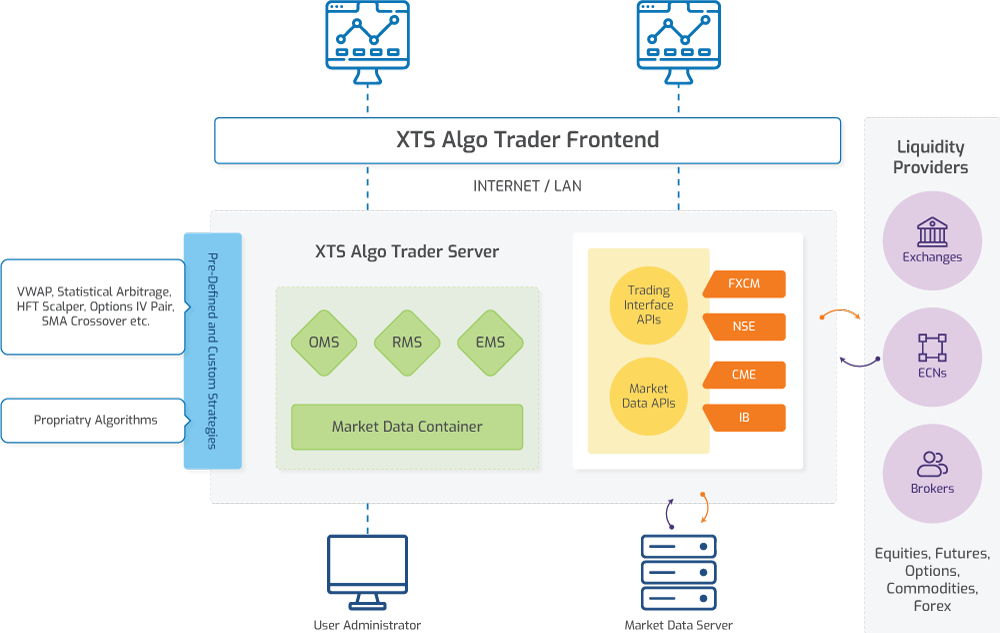

XTS Algo Trader is next generation, most powerful and flexible algorithmic trading platform for quantitative hedge funds, investment bank, prop desk and professional quant developers for rapid development, testing and deployment of simple to sophisticated trading strategies into constantly evolving financial marketplace. It is designed to increase trading execution efficiency and profitability by capturing alpha.

XTS Algo Trader combines powerful features such as, multi-asset trading across multiple liquidity venues from your algorithmic trading strategies with comprehensive risk management system to ensure safety and soundness of your financial systems. It manages end-to-end automated trading lifecycle including market data feed, risk management, order management system, order routing and deliver exceptional trading experience with extensive range of advance features.

Have Trading Ideas?

Build Your Strategy using XTS

Debug and Test with live and simulated market data

Fine tune your strategy, Calibrate parameter and retest

Execute (Go Live)

Symphony Fintech is innovative technology firm with more than 10 years of experience in delivering cross asset front-to-back trading solutions for the financial market participants...

Global Multi Exchange, Multi

Asset Trading

High performance and Low

latency architecture

Powerful Strategy Development

OEMS and Risk Management

Develop and Run any type

strategies models

Third Party Decision system

Integration

Customization Front End

Full source code options for Financial Institutions

and Hedge Fund

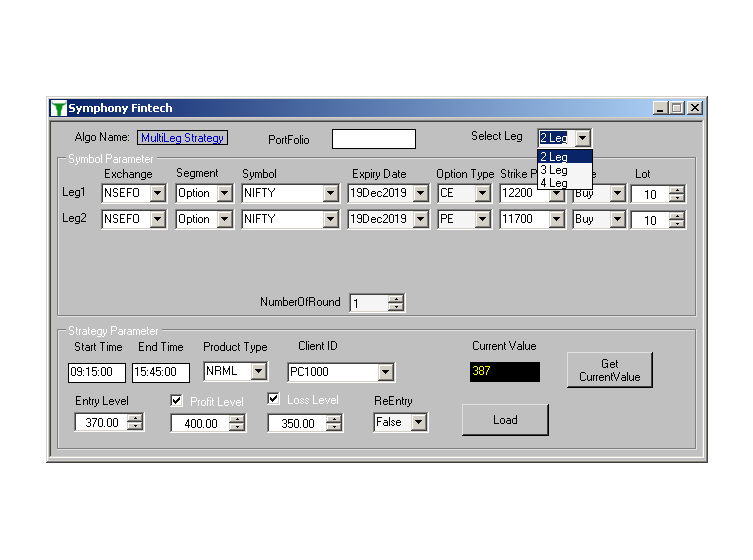

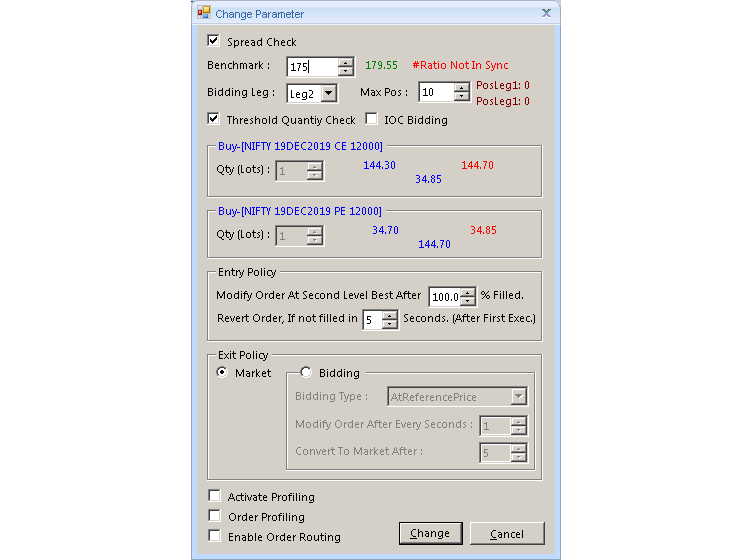

XTS Algo Trader Multi Leg Strategy is designed for smart traders to trade with multiple scripts and get the desired spread. This strategy is capable to place order for 2 leg, 3 Leg and 4 Leg of Options and Futures strategies. This strategy can be used for executing Option strategies, Future-Future, Future –Option, Pair Trading and Rollover.

Two-legged option strategies refer to options strategies with two legs, or component options contracts like Straddle, Strangle etc. User need to define desired Spread as a Benchmark, strategy bid in one leg and try to accumulate second leg once first leg get executed.

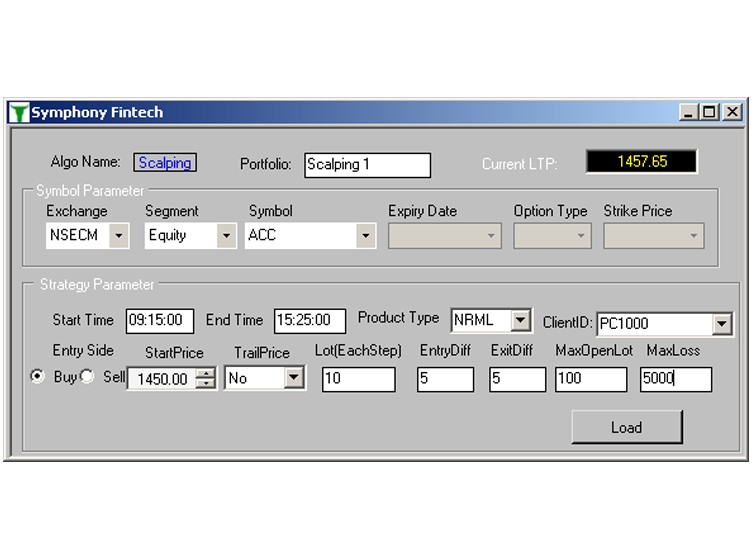

In this strategy whenever price moves down side it will buy/accumulate and upside sell and vice versa. User can define Start point and entry difference & exit difference, so system keep on Buying defined quantity whenever price goes down and sell whenever price moves up automatically and try to accumulate profit.

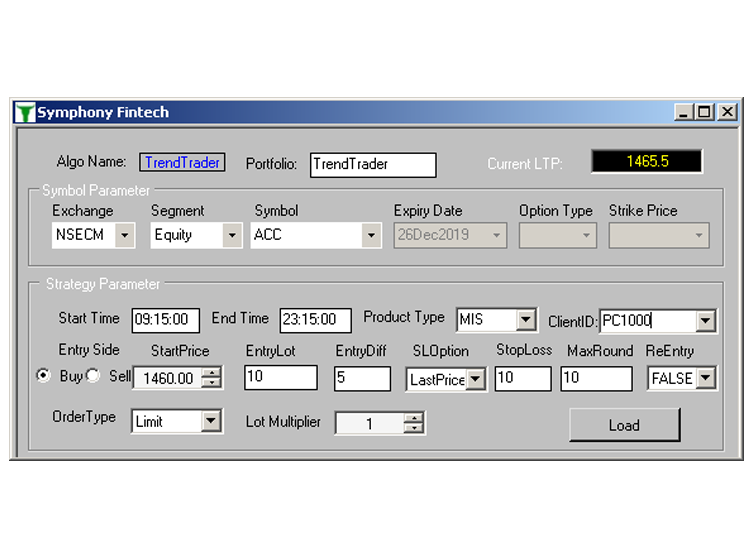

In this strategy whenever price moves in favour it will start accumulating in every defined price interval and place Stop Loss and trail the Stop Loss User can define Start point and entry quantity & entry difference, so system keep on Buying defined quantity whenever price goes upward

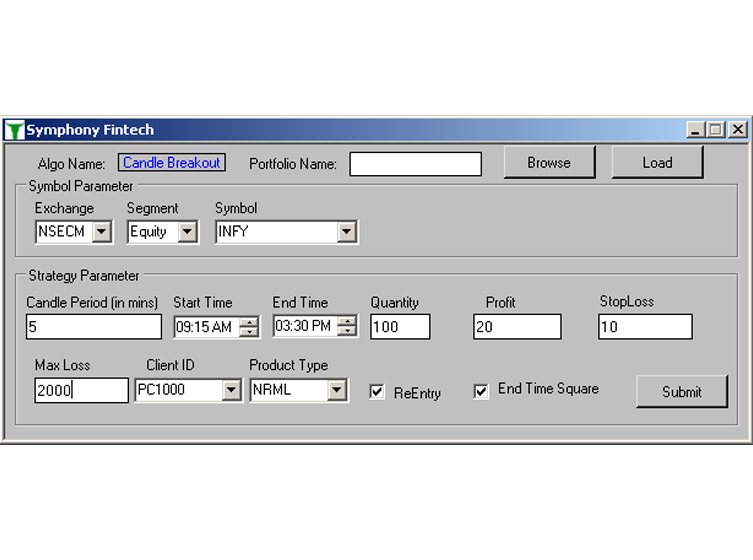

In this strategy system captures the High & Low in given period of time of a candle and place the Buy order 1 tick above the High and Sell order 1 tick below the low of the candle. If any one side order get execute system immediately cancel other side order and place Profit Target and Stop Loss as defined by user.

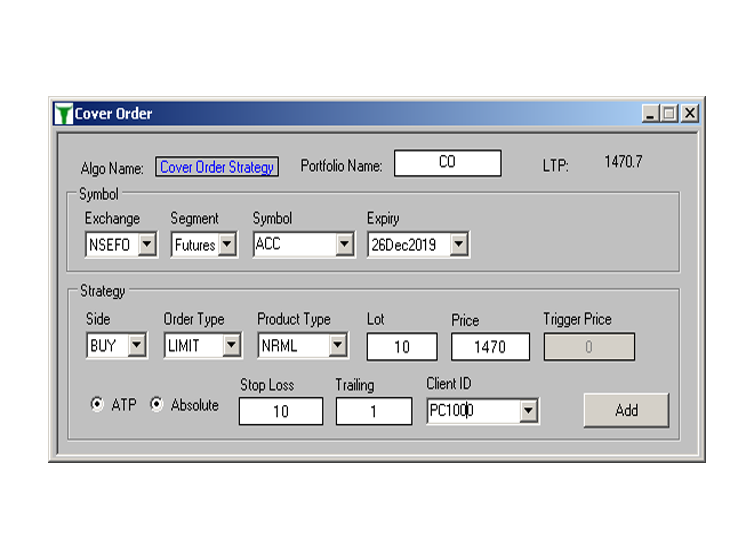

Cover Order is an execution strategy, where user can enter a new position along with a Stop Loss order. As soon as the main order is executed the system will place Stop Loss. System allow user to Trail the Stop Loss when price moves in favour.

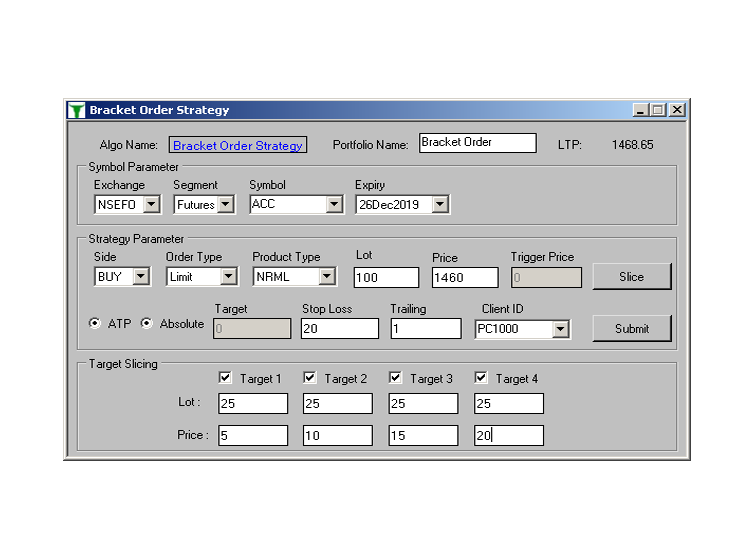

Bracket Order Strategy an execution strategy, where user can enter a new position along with a Target/Exit and a Stop Loss order. As soon as the main order is executed the system will place two more orders (Profit taking and Stop Loss). When one of the two orders (Profit taking or Stop Loss) gets executed, the other order will get cancelled automatically

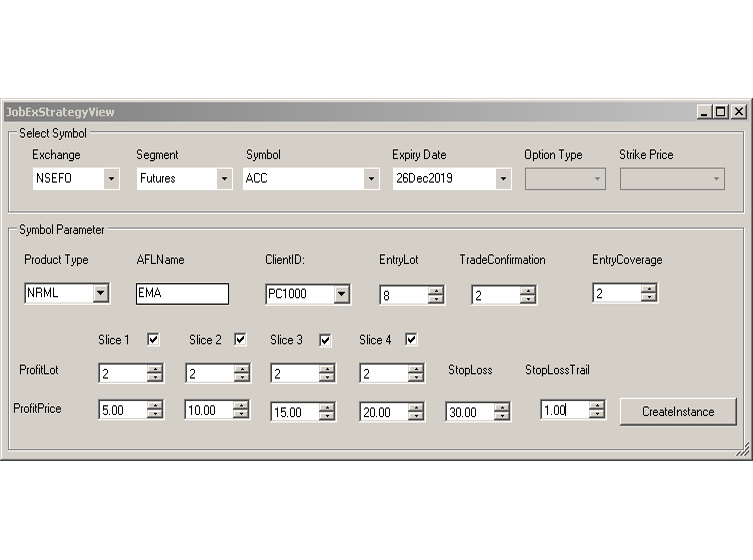

XTS Algo Trader Jobex is a multi client trade execution strategy, which helps trader to intelligently execute Entry-Exit into the market. This strategy has the capability to accept triggers from third-party applications like Amibroker charting software for Intraday & Positional trading. You will be able to do effective trade management for multiple client accounts based on single or multiple Entry trigger from multiple logics.

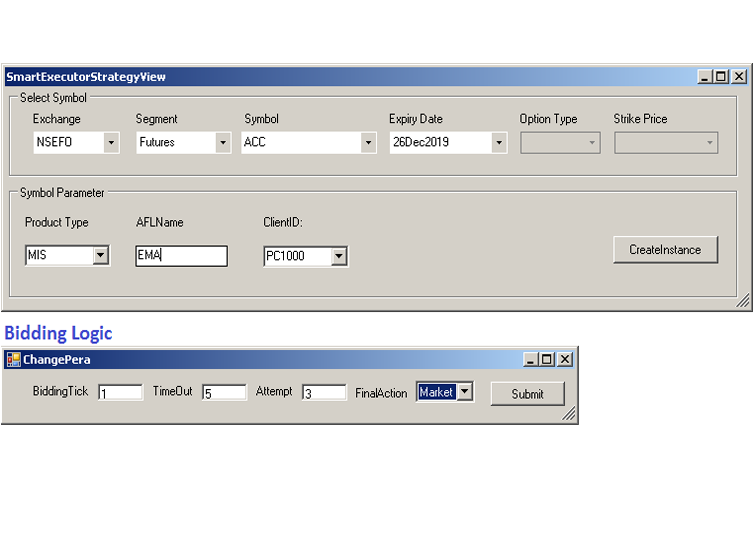

Smart Executor is a multi client trade execution strategy, which helps trader to intelligently execute Entry-Exit into the market. This strategy has the capability to accept triggers from third-party applications like Amibroker charting software for Intraday & Positional trading. You will be able to do effective trade management for multiple client accounts based on single or multiple Entry trigger from multiple logics. This strategy helps to Buy or Sell with time and price based bidding logic.

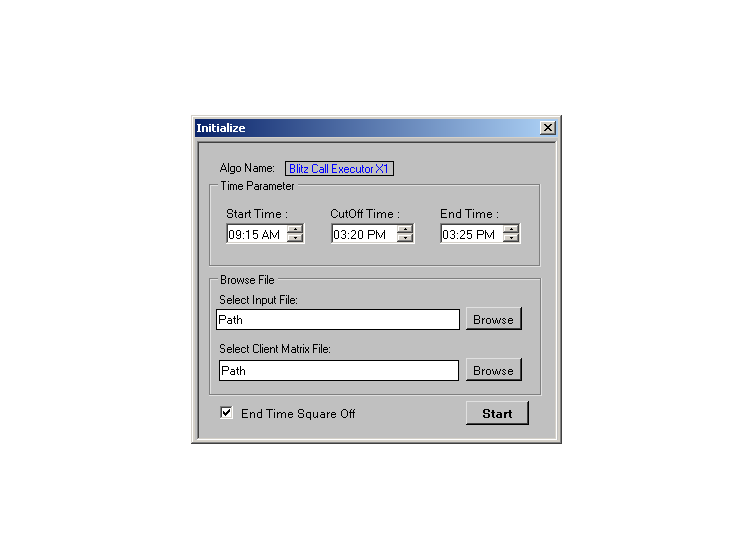

XTS Algo Trader Call Executor is CSV/Excel based Execution strategy for traders who generate Entry/Exit or Buy/Sell levels through their own analytic or subscribe to signal providers for Buy/Sell decisions. Through this strategy user will simply provide the trigger levels in a .CSV file & the strategy will accordingly execute the signals automatically.

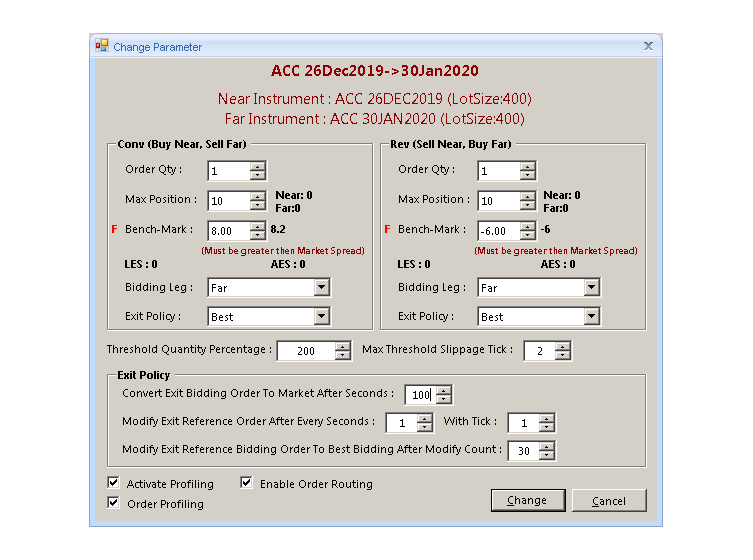

Calendar Spread strategy involves simultaneously buying and selling of future contracts of same symbol but with different expiry dates

Design rich custom trading user interface and build semi automated or manual trading tools suiting your trader requirements

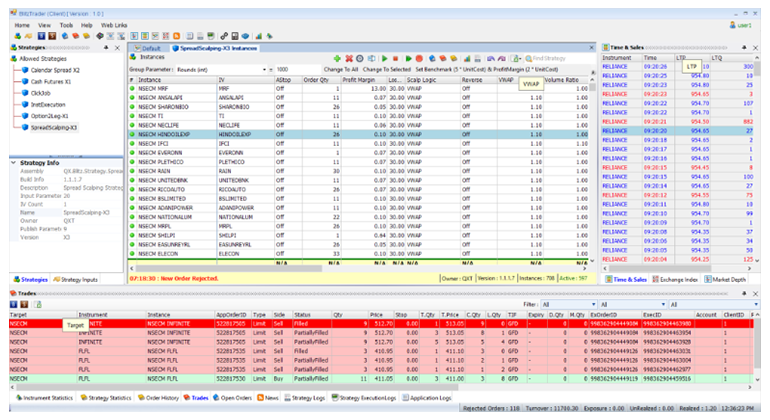

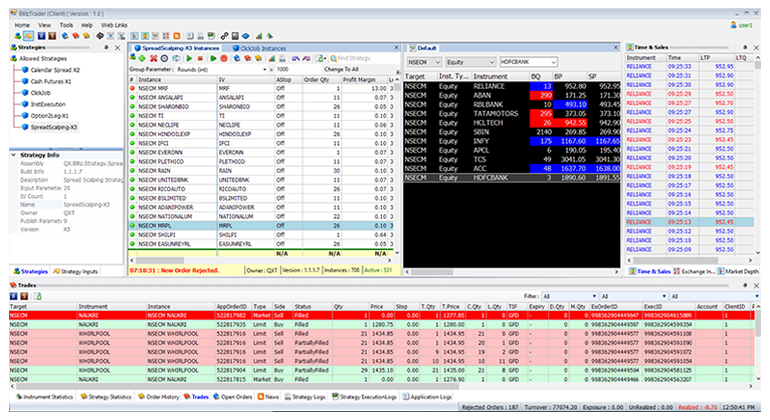

Once you have developed strategy and host it in XTS Algo Trader server with required admin permission, the designated algo trader can create strategy portfolio, launch, control and monitor the live strategy through an Algo Dashboard

Algorithmic trading strategies that are being successfully modeled and in production used today using XTS Algo Trader

High Frequency trading models

High Frequency trading models

HFT scalping strategy employs a very short holding period position based on certain alpha predicting small price movement and exit based on profit target and stop loss. It includes exploiting various price gaps caused by bid/ask spreads and order flows.

Quote based strategies to exploit short lived inefficiency in market i.e. Box spread, Conversion-Reversal, Butterfly Spread, Volatility spread, Cash and Carry Arbitrage in Futures etc

Implied Volatility (IV) based Bidding. This Algorithm allows bidding on Option Instrument based on user defined Implied Volatility (IV) and hedges it in Equity/Future/Options

Arbitrage opportunities across related instrument in different exchanges.

Low Latency Statistical Arbitrage

Low Latency Statistical Arbitrage

Mean Reversal strategy that identifies medium and long term opportunities used to exploit financial markets that are out of equilibrium and assumes prices will eventually adjust to and reflect the fair value with certain predictability. It mostly uses pair trading and uses the concept of equilibrium of oscillation of long and short positions and applies a set of rules to spot inefficiencies and produce return.

Profit situation arising from pricing inefficiencies between securities that is identified through mathematical and statistical modelling techniques.

Index arbitrage: Trading Index against a basket of its component stocks.

Market Making

Market Making

Market making refers broadly to trading strategies that seek to profit by providing liquidity to other traders while avoiding accumulating a large net position in a stock. In the simplest terms, a market maker helps facilitate the execution of a trade by providing a continuous bid-and-ask market for a futures or options contract to any interested party, hoping to make a profit by exploiting the difference between the two prices, known as the spread. Intuitively, a market maker wishes to buy and sell equal volumes of the instrument (or commodity), and thus rarely or never accumulate a large net position, and profit from the difference between the selling and buying prices. Market making often requires placing and cancelling lot of orders and BlitzTrader SmartOrder command enables quant developer to effectively place new, modify and cancel orders at desired price level

Quant Based Algorithm

Quant Based Algorithm

Mechanical Trading Strategies: A lot of best traders use some kind of mechanical rules based on technical analysis in their trading strategies. The trader should follow these rules exactly without hesitation or emotions and rules utilising multiple technical indicators to help them to identify price trends and future trading opportunities. Technical analysis is a form of trading strategy that looks purely at historical price action to determine current and future price trends. Examples: Fibonacci analysis, trend, momentum, volatility and volume based strategies using indicators like SMA, MACD, RSI stochastic, Bollinger Band, ATR, Standard Deviation etc

Market and NewsEvent based Strategy

Market and NewsEvent based Strategy

Several investment management companies have specialized in exploiting news driven trading strategies that would affect the future sock price. Event driven hedge funds need to be on constant alert on news and company press releases as any potential profits could be “arbitraged” away after a short period after the event has taken place. Many news agency providers also provides low latency machine readable news feed that can be directly used in XTS Algo Trader trading strategy to exploit sudden price movement.

Such corporate news events are for example mergers, restructuring, litigation or bankruptcy, product announcements, examples for market news are announcements of economic indicators (unemployment rate, PMIs, etc.) or interest rate changes

Benchmark-Driven Executions Algorithm

Benchmark-Driven Executions Algorithm

Benchmark-Driven strategies seek to minimize slippage relative to client chosen benchmark to improve execution performance while minimizing market impact cost. Algorithms will attempt to find the best available price in the market, which often depends on minimising market impact by concealing a large order as far as possible. Techniques to achieve that often involve slicing an order into many smaller chunks. Examples: VWAP, TWAP, POV etc.

The execution can focus multi-venue in order to cope with the fragmentation of modern financial market and the system is designed to trade on any available source of liquidity